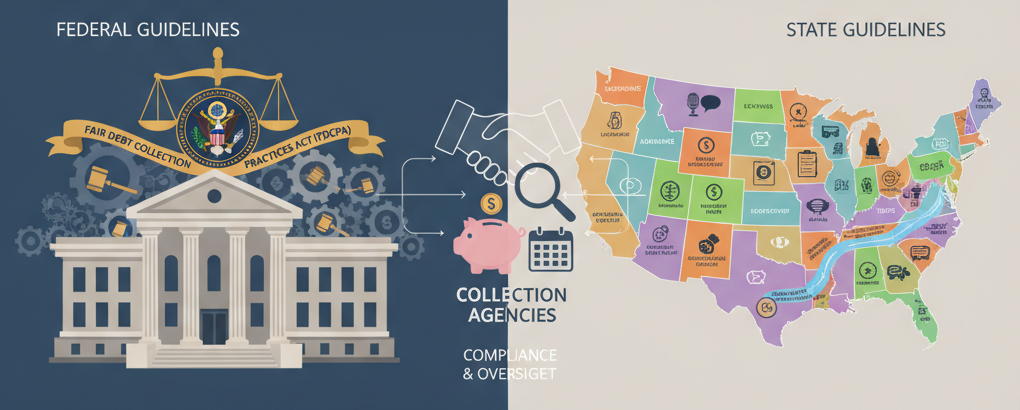

A Closer Look at How Collection Agencies Work Within Federal and State Guidelines

Debt collection agencies are often viewed through a narrow lens, as the intermediaries chasing overdue payments. But the reality is far more complex. Today’s recovery professionals operate under a sophisticated web of federal and state regulations that shape every phone call, email, and report.

These guidelines aren’t optional; they form the backbone of ethical, transparent, and lawful collection. The agencies that follow them not only recover more effectively but also help rebuild trust between businesses and consumers.

At Spire Recovery Solutions (SRS), compliance isn’t just a department; it’s part of the company’s DNA. Every action is designed to meet legal standards while maintaining the dignity of everyone involved.

This blog takes a closer look at how modern collection agencies work within these guidelines, what those laws actually require, and how Spire Recovery Solutions leads the way in compliance-driven debt recovery.

Understanding the Legal Landscape of Debt Collection

The collection industry operates under multiple layers of regulation. Federal laws set the national standard for consumer protection, while state laws add specific licensing and procedural requirements. Together, these frameworks define exactly how agencies can contact consumers, manage data, and report results.

To comply successfully, agencies must combine legal expertise, rigorous training, and real-time oversight, a balance that Spire Collection Agency has mastered.

Why Regulation Exists

Debt collection affects millions of Americans each year. Without oversight, unethical practices could easily emerge, including harassment, misinformation, and privacy breaches among them.

Federal and state governments established collection regulations to:

- Ensure fair treatment of consumers.

- Promote transparency in communication and documentation.

- Protect creditors and agencies from legal disputes.

- Maintain trust in the financial system by holding all parties accountable.

These laws aren’t barriers; they’re blueprints for professionalism.

Federal Regulations That Govern Debt Collection

Federal oversight provides the foundation for all ethical recovery operations. Several major laws define how agencies like Spire must operate day to day.

-

Fair Debt Collection Practices Act (FDCPA)

The FDCPA, enacted in 1977, remains the cornerstone of consumer protection in debt collection. It governs every form of communication between collectors and consumers.

Key FDCPA requirements include:

- No calls outside 8 a.m. to 9 p.m. (consumer’s local time).

- No contact at workplaces if the employer prohibits it.

- Prohibition of threats, abuse, or misleading statements.

- Mandatory written validation notice outlining debt details and rights.

Violations can result in severe penalties, not just for agencies but also for their clients. That’s why Spire trains every collector extensively on FDCPA compliance before they handle live accounts.

-

Fair Credit Reporting Act (FCRA)

This law regulates how consumer debt information appears on credit reports. Agencies must ensure absolute accuracy when furnishing data to credit bureaus.

Spire’s system cross-checks every record before submission and promptly corrects any reported errors. This protects consumers’ credit health while ensuring transparency for clients.

-

Consumer Financial Protection Bureau (CFPB) Rules

The CFPB issues additional guidance, particularly around digital communications such as email, SMS, and social media. Agencies must obtain consent and avoid over-communication or privacy violations.

Spire’s approach: Using compliant digital tools that track consent, limit frequency, and log every message for audit-ready traceability.

-

Telephone Consumer Protection Act (TCPA)

This law governs the use of auto-dialers, prerecorded messages, and text communications. Violations can lead to fines of up to $1,500 per call.

Spire uses secure dialling systems that require manual initiation and adhere strictly to TCPA rules.

-

Gramm-Leach-Bliley Act (GLBA)

When dealing with financial data, agencies must safeguard sensitive consumer information. GLBA mandates encryption, restricted access, and privacy disclosures.

Spire implements advanced cybersecurity protocols, ensuring that client and consumer data are always protected.

By embedding all these federal standards into daily operations, Spire transforms compliance from a checklist into a company-wide discipline.

State Regulations: Adding Another Layer of Accountability

While federal laws establish the baseline, each state adds its own regulatory layer, often requiring specific licensing, disclosures, or consumer protections.

Spire operates nationwide with a full understanding of these regional nuances, ensuring every action aligns with the laws of the state in which the consumer resides.

Licensing Requirements

Many states require agencies to obtain a debt collection license. Each license comes with renewal procedures, bond requirements, and reporting obligations.

Spire maintains all active licenses across the states it serves, continuously monitoring updates to ensure uninterrupted compliance.

Communication Restrictions

Some states impose stricter contact limits or mandate additional written notices. For example:

- North Carolina and Massachusetts regulate call frequency more tightly.

- California requires specific disclosure language in communications.

- New York mandates documentation that verifies the debt before collection begins.

Spire’s compliance department maintains a database of all these requirements, automatically tailoring each contact strategy based on the consumer’s state.

Statutes of Limitation

Each state also defines how long a debt can legally be collected, known as the statute of limitations. Attempting to recover after this period can be unlawful.

Spire’s data systems automatically flag accounts nearing or exceeding those limits, ensuring no expired debt is pursued.

State Consumer Protection Acts

Several states have local laws mirroring or expanding upon the FDCPA. These acts often carry additional penalties for violations.

By maintaining relationships with regional legal counsel, Spire stays informed about evolving legislation and court precedents, preventing compliance issues before they arise.

How Collection Agencies Build Compliance Into Their Operations

Complying with these laws isn’t just about knowing them; it’s about integrating them into every workflow, system, and conversation.

Spire Recovery Solutions follows a compliance model built around four pillars: education, technology, monitoring, and documentation.

-

Education and Training

Every collector undergoes intensive onboarding focused on:

- FDCPA/FCRA guidelines.

- State-specific licensing requirements.

- Communication etiquette and tone.

- Data privacy and cybersecurity awareness.

Training continues monthly, with updates whenever new regulations are introduced.

-

Technology and Automation

Spire’s proprietary collection software automates compliance tasks, such as:

- Real-time call recording and review.

- Consent tracking for digital communication.

- Documentation timestamps for every action.

- Automated disclosure inclusion in written notices.

This automation reduces human error while maintaining a transparent audit trail.

-

Monitoring and Quality Assurance

Supervisors regularly audit collector interactions. Calls are monitored live and post-recorded for review, ensuring tone, accuracy, and compliance consistency.

Any deviation triggers immediate retraining or corrective action, reinforcing a culture of continuous improvement.

-

Documentation and Record-Keeping

Every communication, payment, and dispute is logged and stored securely. This protects both consumers and clients while ensuring full traceability for audits or legal proceedings.

Together, these systems make compliance an everyday function rather than a reactive fix.

The Consumer’s Perspective: Rights and Protections

Regulations don’t just guide collectors; they empower consumers. Understanding these rights helps consumers engage confidently in the resolution process.

-

Right to Verification: Within five days of first contact, collectors must send a written validation notice confirming key details of the debt.

-

Right to Dispute: Consumers have 30 days to dispute the debt’s accuracy. Spire halts all collection activity until the verification process is complete.

-

Right to Privacy: Collectors cannot discuss debts with anyone other than the consumer, their attorney, or a legally authorised party.

-

Right to Respectful Treatment: Abuse, threats, or deceptive practices are strictly forbidden. SRS enforces a zero-tolerance policy against such behaviour.

By honouring these rights, Spire helps consumers rebuild trust and take control of their financial situations without fear or intimidation.

The Client’s Perspective: Why Compliance Matters

For Spire’s business clients, from banks to hospitals, partnering with a compliant agency protects reputation and revenue alike.

Benefits of strict adherence include:

- Fewer consumer complaints and disputes.

- Reduced legal exposure and regulatory scrutiny.

- Stronger consumer engagement and faster recoveries.

- Enhanced brand image built on transparency and respect.

Compliance isn’t just a legal shield; it’s a competitive advantage. Clients who choose ethical agencies like Spire see better results because consumers are more willing to cooperate when treated fairly.

The Technology Behind Regulatory Compliance

Modern compliance depends heavily on technology, and Spire has invested in advanced systems that combine efficiency with oversight.

Automated Compliance Checks

Every action is cross-verified against regulatory frameworks. If a collector attempts contact outside allowed hours or forgets a required disclosure, the system flags it immediately.

Data Encryption and Secure Storage

All consumer and client data are stored in encrypted databases that meet or exceed federal cybersecurity standards.

AI-Driven Pattern Analysis

Artificial intelligence reviews thousands of call logs to detect language or tone patterns that could indicate potential violations, allowing proactive coaching.

Real-Time Reporting Dashboards

Clients receive access to dashboards displaying collection progress, compliance metrics, and consumer satisfaction data. This transparency reinforces accountability.

Technology doesn’t replace empathy; it enhances it. By removing administrative burdens, collectors can focus on listening, understanding, and helping.

Why Compliance and Ethics Drive Better Results

Many assume compliance limits productivity. Spire’s experience proves the opposite.

-

Higher Consumer Engagement: Consumers respond more positively to transparent, respectful communication. This leads to more completed arrangements and faster resolutions.

-

Lower Legal Risk: Each compliant interaction reduces potential lawsuits, fines, or disputes, protecting both agency and client.

-

Better Client Retention: Ethical practices strengthen client relationships, encouraging long-term partnerships built on mutual trust.

-

Sustainable Performance: Compliance creates consistency. When every collector follows the same rules and processes, performance remains steady and predictable.

By marrying ethics with efficiency, Spire shows that compliance isn’t a constraint; it’s a catalyst for success.

Building a Culture of Accountability

The best compliance programs come from the top down. Leadership at Spire Recovery Solutions reinforces accountability through:

- Transparent communication channels.

- Regular compliance meetings.

- Recognition programs for collectors with exemplary adherence.

- Immediate escalation and resolution for consumer complaints.

This culture ensures that every collector understands one core truth: compliance isn’t just about avoiding penalties, it’s about doing what’s right.

Conclusion

The world of debt collection operates under some of the most detailed regulations in business, and for good reason. These laws ensure that every recovery effort respects both the creditor’s rights and the consumer’s dignity.

A truly professional agency doesn’t just follow the rules; it builds its identity around them. That’s what sets Spire Recovery Solutions apart. As a spire collection agency, it combines legal precision, ethical communication, and advanced technology to deliver results that stand up to scrutiny at every level.

From federal mandates like the FDCPA and FCRA to the nuanced licensing requirements of individual states, Spire’s operations are designed to exceed compliance expectations, not just meet them.

For businesses seeking a recovery partner that values integrity as much as performance, and for consumers who deserve fairness in every interaction, Spire represents the gold standard of ethical debt collection.